Financial Planning | Investing | Personal Finance | Article

7 Insurance Myths You Must Not Believe

by Ooi May Sim | 8 Feb 2024 | 6 mins read

No one can predict what will happen tomorrow. The only thing you can do is to plan and prepare for unforeseen circumstances financially, so it doesn’t damage your savings and leave you reeling in debt. Insurance is one way to protect yourself from financial loss as it acts as a financial safety net during health and medical emergencies.

However, there’s a lot of misinformation about insurance out there, causing many to make poor insurance decisions that could lead to long term repercussions.

Equip yourself to make better, more informed decisions about insurance as we demystify some common insurance myths for you.

Myth 1: Insurance is expensive so I can’t afford it

Truth: Insurance doesn’t have to be costly and can be tailored to fit your budget. But there are some factors that can directly affect how much your insurance will cost, such as your age, gender, lifestyle factors and current health status.

Insurance premiums are generally lower if you are younger and healthier as compared to if you only decide to purchase insurance when you are older or have existing health issues. This is because you pose less of a financial ‘risk’ to insurance agencies.

Hence, it’s good to start considering insurance when you are still young and healthy to keep your insurance costs low.

Myth 2: I can pay for my own medical needs without insurance

Truth: Some people question the need for insurance because they believe that the money saved from not having insurance is enough to cover their medical needs. Unfortunately, with medical costs on the rise annually (medical inflation was at 16.2% in 2022), this may not be the case. Let’s look at an example together.

If you get an insurance policy that costs RM200 a month and you have been paying for it for the past 20 years, you would have spent RM48,000 on insurance. That’s not a small sum of money.

However, it is still cheaper than what a coronary bypass cost. With heart disease being the leading cause of death in Malaysia, if you need a coronary bypass surgery, this could cost you up to RM80,000 at a private hospital. As you can see, this is much higher than the accumulated insurance premiums you would have paid for 20 years. And this just the estimated cost now and is bound to be more expensive in 20 years!

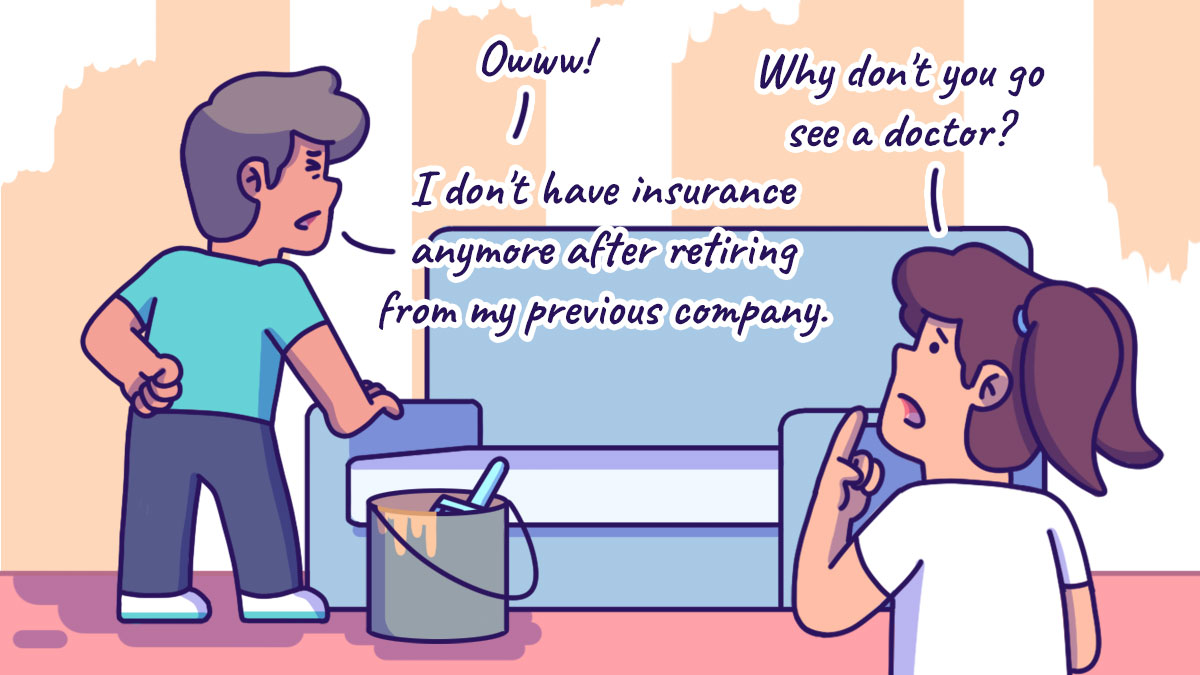

Myth 3: My company provides insurance for me so I don’t need another policy

Truth: Although your employer may offer medical insurance, the plan may be minimal and may not be sufficient to cover your needs. If you need any additional medical attention or any upgrades, you’ll have to pay for it on your own.

Also, a corporate insurance plan is only valid when you are employed with the company. As soon as you leave the company or retire, your policy will be void and you will no longer be able to claim from the insurance. This poses a problem, especially during your retirement where you may have higher medical expenses to pay for.

It is advisable for you to supplement your employer insurance coverage with one of your own that is catered to your specific needs. Having your own policy ensures that you are covered throughout your lifetime, or at least until a specific age (please read your policy).

Related

Myth 4: I don’t need insurance because I’m young and healthy

Truth: This is not entirely wrong as you tend to have less health problems when you are young compared to when you are older. But this is also why your premiums cost less.

The cost of insurance, especially life insurance, tends to increase with age. By signing up for a policy when you are young and healthy, you will be locking in your insurance at that lower rate, which can save you money in the long run.

Myth 5: I can buy health insurance when I need it

Truth: Insurance companies are smarter than you think. Whenever you sign up for a policy, you’ll have to go through a waiting period before the policy takes effect. Hence, it could take weeks or months before you are able to make a claim for the illness you have.

Also, if you sign up for a policy after you have been diagnosed with an illness, it will be deemed as a pre-existing condition, and you won’t be allowed to make any claims that fall under this condition.

Related

Myth 6: All my medical needs will be covered if I have health insurance

Truth: Unfortunately, health insurance doesn’t cover every medical condition out there. Your policy will state the specific conditions that are covered and if you suffer from an illness that is not on the list, you’ll have to foot the medical bill on your own.

Some policies also don’t cover outpatient treatments and annual check-ups such as blood tests, so you’ll have to set aside your own money for these medical expenses.

On top of that, many people tend to confuse the different types of insurance available. This may pose a problem because they may have one type of insurance thinking they are covered for everything, but in reality, they aren’t.

For example, someone who has a personal accident policy can be compensated in the event of an injury but is not covered if they have an illness such as heart disease. So, it is important that you understand what insurance you are getting and what is covered in the policy before you sign up for it.

Your insurance is also invalid outside of the country you are insured in, unless you opt for international coverage. That’s why you’ll see travel insurance being offered whenever you buy flight tickets or travel packages. These policies often cover medical fees for personal accidents and inconveniences such as trip cancellations and baggage delays.

Myth 7: All insurance policies are the same

Truth: Even if you and a friend sign up for the same insurance package, both your policies can vary from each other. From coverage, exclusions and terms, every policy is catered to the person who bought it.

For instance, if you are a smoker, your premiums would be higher than someone who doesn’t smoke because you have a higher health risk. There are certain medical claims that you might be excluded from as well.

It is important to note that every insurance policy varies in their benefits, terms and conditions and costs, so remember to do your research and find an insurance policy that fits all your needs before signing up for one. And don’t let these insurance myths sway your decisions.